Conventional Loans: Pros, Cons, and Who They're Best For

Conventional Loans: Pros, Cons, and Who They're Best For

When you're ready to buy a home in Ocala, you'll quickly discover that the mortgage world has more options than a Starbucks menu. But here's the thing: conventional loans are like the classic latte of home financing: they're the most popular choice for a reason, and they might just be perfect for you.

Let's break down everything you need to know about conventional loans, from their biggest advantages to potential drawbacks, so you can decide if this financing route makes sense for your Ocala home purchase.

What Exactly Is a Conventional Loan?

Think of a conventional loan as the "vanilla" mortgage option: not because it's boring, but because it's the standard that everything else gets compared to. Unlike FHA, VA, or USDA loans, conventional mortgages aren't backed by the government. Instead, they're issued by private lenders like banks, credit unions, and online mortgage companies.

Most conventional loans follow guidelines set by Fannie Mae and Freddie Mac, two government-sponsored enterprises that buy mortgages from lenders. This standardization helps keep interest rates competitive and makes the loans easier to sell on the secondary market.

The Sweet Benefits of Conventional Loans

Lower Down Payment Than You Think Contrary to popular belief, you don't need 20% down for a conventional loan. You can actually get started with as little as 3% down on a fixed-rate mortgage or 5% on an adjustable-rate loan. In Ocala's current market, where the average home price hovers around $317,000, that's roughly $9,500 to $15,850 to get your foot in the door.

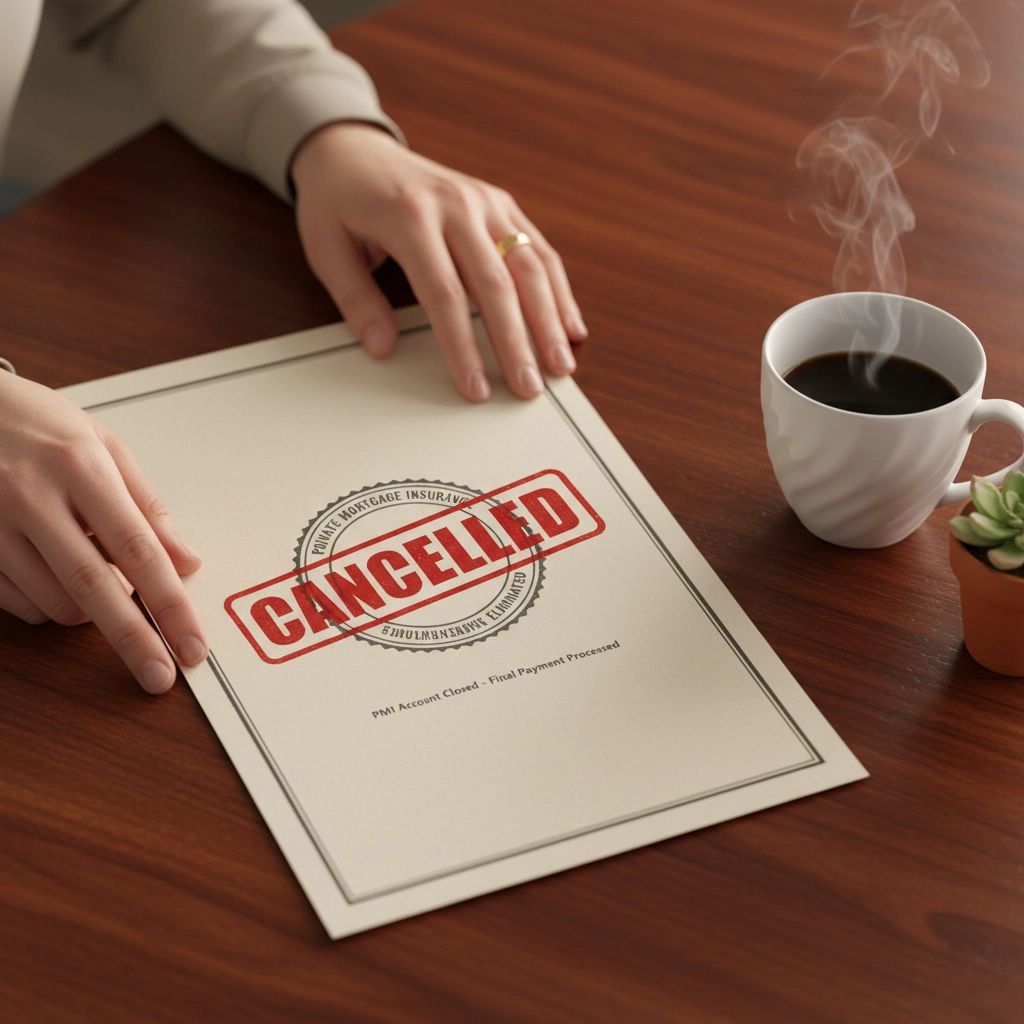

Say Goodbye to Mortgage Insurance (Eventually) Here's where conventional loans shine: once you reach 20% equity in your home, you can kiss that private mortgage insurance (PMI) goodbye. Unlike some government-backed loans where mortgage insurance sticks around for the life of the loan, conventional loans let you cancel it. With Ocala's appreciation trends, many homeowners find themselves hitting that 20% mark sooner than expected.

Flexibility Is the Name of the Game Want to buy a primary residence? Check. Thinking about an investment property? You're covered. Dreaming of a vacation home? Conventional loans can handle that too. This flexibility makes them incredibly popular with Ocala buyers who are looking at everything from downtown condos to horse properties in the surrounding areas.

Faster Processing Times Without all the government red tape and additional inspections required by government-backed loans, conventional loans typically move through the approval process more quickly. In a competitive market like Ocala, where good properties can get multiple offers, this speed advantage can be crucial.

Higher Loan Limits Conventional loans can go higher than most government-backed options. In Florida, conforming loan limits allow you to borrow up to $806,500 in most areas, which gives you plenty of room to explore Ocala's luxury home market if that's where your heart (and budget) leads you.

The Not-So-Great Parts

Credit Score Requirements Are Real You'll need a minimum credit score of 620 to qualify, and honestly, that's just the bare minimum. To get the best interest rates, you'll want to be closer to 750 or higher. If your credit needs some TLC, you might want to consider other options first or spend some time boosting your score.

Interest Rates Can Vary While conventional loan rates are generally competitive, they're not always the lowest option available. Your specific rate depends on your credit score, down payment, debt-to-income ratio, and current market conditions. Sometimes government-backed loans offer better rates for certain borrowers.

Stricter Income Documentation Lenders want to see stable, verifiable income, and they're thorough about it. If you're self-employed, have irregular income, or recent job changes, the documentation requirements can feel overwhelming. They typically want your debt-to-income ratio to stay below 45%, though some lenders will go up to 50% in certain situations.

Past Financial Hardships Take Time If you've experienced bankruptcy or foreclosure, conventional loans require longer waiting periods compared to some government options. You'll typically need to wait two to four years after bankruptcy and three to seven years after foreclosure before qualifying.

Who Should Consider Conventional Loans?

The Steady Eddie Borrower If you have stable employment, a decent credit score (620+), and can document your income easily, conventional loans are probably your best friend. They're designed for borrowers who fit the traditional lending profile.

Property Investors and Second Home Buyers Planning to buy rental property in Ocala's growing market? Conventional loans are often your only option for investment properties. The same goes for vacation homes: government-backed loans typically require the property to be your primary residence.

Those Who Want PMI Flexibility If you're putting down less than 20% but expect to build equity quickly (either through appreciation or extra payments), the ability to cancel PMI makes conventional loans very attractive.

Higher-End Home Buyers If you're looking at properties above the government loan limits, conventional loans can handle higher purchase prices without jumping into jumbo loan territory immediately.

Getting Started with Conventional Loans in Ocala

The application process is straightforward, but preparation is key. You'll need:

• Credit score of 620 minimum (750+ for best rates) • Down payment of 3-5% depending on loan type • Stable employment history (usually 2 years) • Debt-to-income ratio below 45% • Documentation of income, assets, and employment • Property appraisal and home inspection

In Ocala's current market, having your pre-approval letter ready before you start shopping is crucial. Properties are moving quickly, and sellers want to see serious buyers who can close on time.

The Bottom Line on Conventional Loans

Conventional loans aren't the flashiest option out there, but they're incredibly solid for the right borrower. They offer flexibility, competitive rates for qualified buyers, and the potential to eliminate mortgage insurance down the road.

Whether you're a first-time buyer looking at starter homes in Ocala or an experienced buyer ready to upgrade to your dream property, conventional loans deserve serious consideration. They're the Swiss Army knife of mortgages: reliable, versatile, and available when you need them.

The key is understanding whether your financial profile matches what conventional lenders are looking for. If you have steady income, decent credit, and can handle the down payment requirements, you're likely in good shape.

Ready to explore your conventional loan options in the Ocala market? The GEMM Team has helped countless buyers navigate the mortgage process and find the financing that works best for their situation. We work with trusted lenders who understand the local market and can guide you through every step of the process.

Don't let financing questions keep you from finding your perfect Ocala home. Reach out to us today and let's discuss how conventional loans might fit into your home buying strategy. Your dream home is waiting, and we're here to help you make it happen.

Categories

Recent Posts

GET MORE INFORMATION